Another Lost Decade for Workers

The rich world is heading for another lost decade of wage stagnation – unless workers figure out how to fight back.

Across the rich world, rising prices are once again eroding workers’ already strained incomes. The immediate catalyst has been Trump and Netanyahu’s senseless war on Iran. But the problem can be traced all the way back to the financial crisis of 2008, which was followed by a lost decade of stagnant real wages.

The 2020s now looks set to be another lost decade of stagnant incomes. First, we had the post-pandemic cost of living crisis, exacerbated by Russia’s invasion of Ukraine. Before the Iran war, inflation looked set to ebb. But the chaos unleashed by Trump’s invasion is going to leave lasting scars on the global economy. And the people who suffer the most will be those least able to bear it.

The first lost decade

In the years following the financial crisis of 2008, the UK endured a decade of stagnation in real wages. With growth and productivity fairly flat, and bargaining power low, workers were not organised enough to demand higher wages. The same problem was evident across much of Europe – particularly southern Europe. The US fared somewhat better, but low-income households were still squeezed.

Ultra-low interest rates – combined with central bank asset purchases – provided something of a salve during this period of stagnation. Many people on relatively low incomes were still able to take out mortgages at low interest rates. Consumers could buy cars and many other consumer goods on credit. And companies backed by cheap borrowing were able to provide them with services on the cheap.

At the same time, easy money led to an increase in asset prices, which increased wealth inequality. The rich were getting richer every year while wages were stagnating. In the UK and Europe, government austerity programmes added insult to injury. And the political turmoil of the 2010s – from Brexit, to the resurgence of democratic socialism, to the rise of the far right – can largely be traced back to this combination of wage stagnation, austerity, and rising inequality.

Still, easy money masked most of these problems – particularly for middle-earning households. Many middle-earners were able to ride the wave of rising asset prices by taking out low interest loans to purchase housing and other assets. When the pandemic hit, central banks doubled down on the new monetary orthodoxy, further slashing rates, leading to cheaper credit and higher asset prices. All this limited the political fallout from stagnation.

The end of easy money

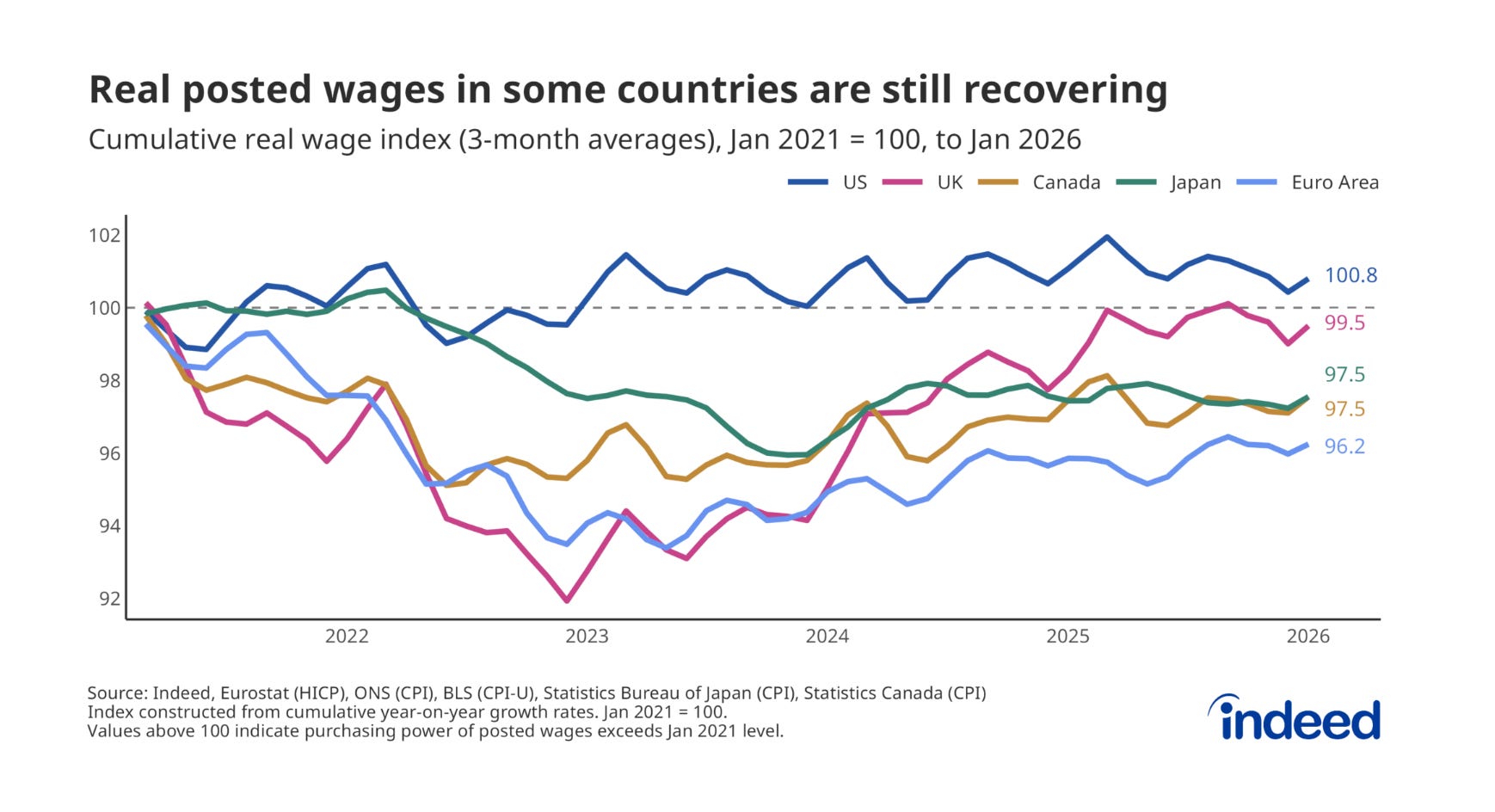

The return of inflation – and the end of low interest rates – revealed the underlying contradictions of a growth model built on low wages, low productivity, and rising inequality. The cost-of-living crisis – or, more accurately, the cost of greed crisis – simultaneously reduced real wages and put an end to the era of easy money. Both low- and middle-income households suffered sharp falls in their living standards as a result.

In the UK, the fall in real wages between 2021 and 2023 was the largest since records began in the nineteenth century. In the United States, real median wages declined for two consecutive years. Across the eurozone, the pattern was the same: workers ran faster and still fell behind.

The households that were hardest hit were those that spend the highest share of their income on energy and food – the basics of material life. These households are, overwhelmingly, those at the bottom of the income distribution. At the same time, profits for the big oil companies, defence, supermarkets and many other sectors boomed. In other words, the last crisis resulted in a significant upward redistribution of wealth.

Central bankers made the problem worse by hiking interest rates to reduce demand, increasing unemployment. They did so with a view to eroding workers’ bargaining power, so they were unable to demand wage increase in line with inflation. As I argued at the time, central bankers made the decision to respond to the cost-of-living crisis by imposing the costs of adjustment on workers. They succeeded.

The end of the era of easy money imposed costs on middle-earning households too. Up to that point, middle earners had been able to ride the wave of rising asset values by taking out low-interest loans – despite their largely stagnant income. From 2021, that path was closed off.

But even if interest rates were now too high to support consumers’ ambitions to asset ownership, they were still too low to take the wind out of the sails of a booming stock market. The AI bubble ensured that the recovery from the pandemic was K-shaped, with huge companies and wealthy households benefitting from the boom, while everyone else was left behind.

The wages of war

Then, Trump decided to invade Iran.

Subscribe to read more - and listen to the full piece via my weekly podcast. Can’t afford it? DM me for a solidarity discount.